The word curtailment – the forced cuts in centralized solar and wind power generation by the National System Operator (ONS) to avoid compromising the grid – has ceased to be a simple side effect of the uneven growth of renewable sources in recent years, without a corresponding increase in grid infrastructure, and has become a source of losses for energy companies that threatens even the giants of the sector.

A study by the consulting firm Volt Robotics showed that the cuts are already affecting the entire sector: Brazil wasted a fifth of the wind and solar energy produced last year (20%), generating losses of R$ 6.5 billion for the 1,500 centralized renewable plants, from small to large, under the supervision of the ONS (National System Operator).

In a report, the Fitch ratings agency estimated that power cuts should reduce Auren Energia 's consolidated EBITDA in 2025 by R$400 million (8% of the total), Serena Geração 's by R$200 million (11%), and Engie Brasil's by R$150 million (2%), based on results recorded up to the third quarter. As the aforementioned giants are still compiling data for the fourth quarter and the consolidated figures for 2025, these numbers may change.

"Strictly speaking, the curtailment effect extends to the entire ecosystem of the electricity sector, beginning to impact the price of energy traded in the free market and the regulated market," says Donato Filho, CEO of Volt Robotics.

He warns that the phenomenon also freezes new projects, increasing the risk of shortages sooner than expected. "The surplus energy that was estimated to last until 2030-2031 could run out by 2028, compromising data center installation plans if adequately structured expansion mechanisms are not created," says Donato Filho.

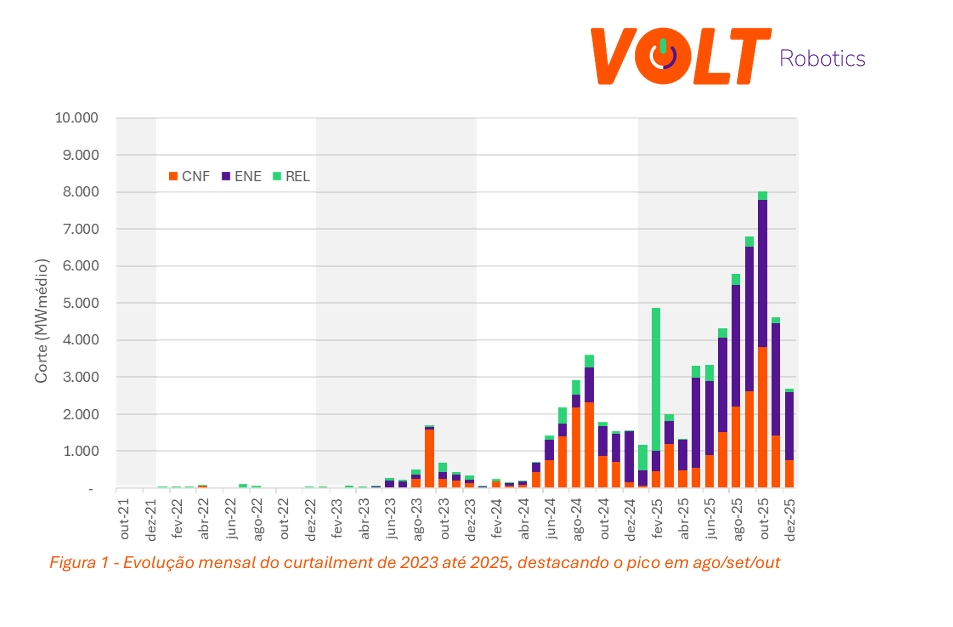

The average number of power cuts compiled by Volt in conjunction with Aneel, the regulatory agency, jumped from 9.6% in 2024 to 20.6% last year, totaling 4,021 average megawatts (MWm) — enough energy to supply 8 million homes. However, the cuts are uneven: solar power plants suffered an average of 35%, compared to 15% for wind farms.

The imbalance stems from the excess of solar generation in the mornings, especially from the micro and mini-distributed generation (MMGD) and distributed generation (GD) segments, whose panels installed on rooftops inject energy directly into the distribution network. Since they are not under the control of the ONS (National System Operator), the centralized power plants end up paying the cost of curtailment .

Although residential solar panels are currently exempt from the cuts, the impact on the sector is evident. Investments in new photovoltaic projects are expected to fall by 40% by 2025.

Portfolio review

Given this scenario, NeoFeed spoke with executives from three giant companies in the sector – Engie Brasil, Auren, and Echoenergia – and all acknowledged the seriousness of the crisis, admitting that they are readjusting their portfolios and revising investment plans in the short and medium term.

The challenge is to adapt the losses caused by curtailment to the complex web of contracts foreseen by the regulated and free energy markets, the most important in the electricity sector. Together, combining consumption and average prices, they generate between R$ 220 billion and R$ 280 billion per year.

The free energy market is an environment where companies can choose from whom to buy electricity and negotiate prices, terms, and volumes directly with generators or trading companies.

When an energy company with a contract to fulfill in the free market suffers curtailment , the impact is direct – the generator needs to buy energy measured in megawatt-hours (MWh) on the spot market, which applies daily rates, generally higher than long-term contracts, on a minimum basis of R$ 200 per MWh.

In the regulated energy market, consumers buy electricity from local distributors, with tariffs set by the government. In this market, the consumer does not choose their supplier: the distributor is responsible for buying the energy and delivering it to the customer. Prices are set by Aneel (the Brazilian Electricity Regulatory Agency) and follow standardized rules. This is the model used by most households and small businesses.

The risk of variation in production (for example, due to lack of wind, water, or curtailment ) in the regulated market is not the generator's, but the buyer's (the distributor). However, if the power plant is not available when called upon, the generator suffers penalties.

The generator receives payment for the energy contract in the first year, even if it doesn't deliver what was promised. However, in the following year, it suffers a "reimbursement" (adjustment to revenue) related to the undelivered energy, often increased (115% of the contractual value, for example).

Fabio Zanfelice, CEO of Auren Energia, states that curtailment usually affects the company's cash flow in both environments. "The revenue mismatch impacts both, but the cash profile differs," he says.

According to him, in 2023, the average PLD (price used in the short-term market to settle differences between what agents contracted and what they actually consumed or generated) was below regulated prices, penalizing those who sold energy in the regulated market more; but recently, the free market has been more expensive.

Zanfelice states that Auren has reduced its exposure to curtailment thanks to the company's portfolio, with 56% of its energy generated by hydroelectric plants and 34% from renewable sources. He also acknowledges the positive result of the so-called hourly mark-to-market effect of hydroelectric generation – a process of economically evaluating, hour by hour, the energy generated by a hydroelectric plant using the prevailing hourly market price (hourly PLD).

“This gives us what we call modulation gain: because of the price distortion, we are able to partially offset the loss we have with curtailment ,” says the executive from Auren, a company that recorded revenue of R$ 3.6 billion in the third quarter of 2025 (the latest available), an increase of 12.8% over the previous year.

Gabriel Mann, director of regulatory affairs at Engie Brasil, states that the company also revised its plans due to the power cuts, updating curtailment projections (25% in 2025, a premise communicated to investors) and refining scenarios for 2028–2029.

“Lower available generation limits marketable energy and increases the need to reserve reserves to honor contracts,” says Mann. “The impact falls more on the energy that could be sold in the future than on that already contracted, thanks to the active management of our portfolio, which is entirely renewable,” he adds.

Wind/solar power accounts for approximately 25% of Engie's total portfolio compared to hydropower. "This composition better withstands curtailment volatility during peak system demand times, such as late afternoon and evening, as hydroelectric generation partially compensates for the reduction in wind/solar power," he adds.

Mann states that Engie avoids last-minute energy purchases thanks to internal reserves. The strategy is to reduce future sales and maintain planned surpluses of contracted energy to cover curtailment , prioritizing predictability and contract fulfillment.

According to him, between 70% and 80% of Engie's wind/solar capacity is in the free market. "In consolidated terms, including hydroelectric generation, Engie's energy portfolio is approximately 60% in the free market and 40% in the regulated market."

With this strategy, Engie Brasil closed the third quarter of 2025 with net operating revenue of R$ 3.3 billion, representing a growth of 10.7% compared to the same quarter of 2024.

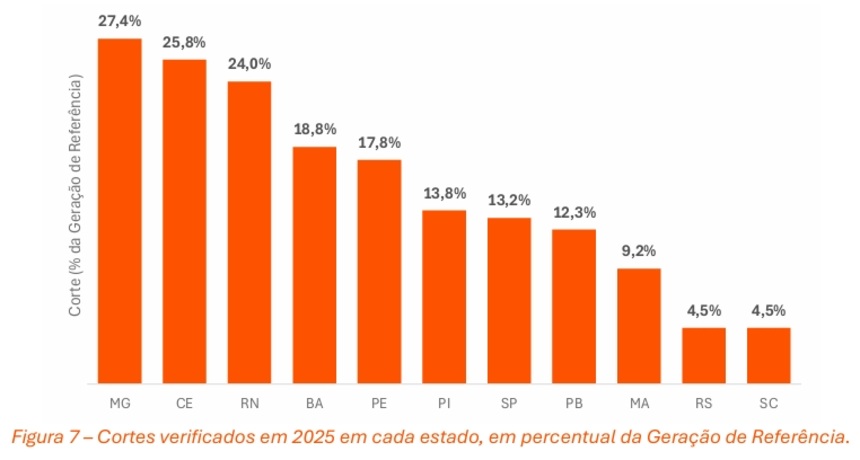

Echoenergia, in turn, ended up suffering more from the curtailment due to its portfolio, consisting of 42 wind power complexes and 23 solar power plants, excluding hydroelectric plants, totaling 484 wind turbines and approximately 1.2 million photovoltaic panels, in states affected by the cuts in centralized generation, such as Alagoas, Bahia, Ceará, Maranhão, Pará, Pernambuco, Piauí, Amapá, and Rio Grande do Norte.

Liu Aquino, CEO of the company, states that the free market impacts immediate cash flow. “With 60% of our energy in the free market, the cuts force PLD (Price of Energy in the Spot Market) replacement within the same month; and with rainfall below expectations and high PLD, the replacement cost was more than double that of last year, severely pressuring cash flow,” explains Aquino, adding that in the regulated market, the 'flow balance' smooths out the cash flow, as the replenishment occurs over time.

Therefore, Echoenergia's operational focus in the short and medium term is on cash flow, not strategy. "The priority is to mitigate the impact on cash flow: seeking commercial optimization, allocating energy to reduce volatility and exposure, as well as strengthening regulatory action with bodies such as Aneel and the Ministry of Mines and Energy, to clarify rules and responsibilities," he emphasizes.

Since 2022, Echoenergia has been part of the Equatorial Energia Group, which operates in the areas of power generation, distribution, as well as telecommunications, services, and sanitation. The results for the third quarter of 2025 refer to Equatorial Energia as a whole, which is the parent company.

NeoFeed has learned from market sources that Echoenergia's losses last year reached R$ 500 million. Aquino does not confirm the figure, but admits that the losses were substantial.

“The group has the cash to invest if necessary,” says the Echoenergia executive. “But smaller companies, which don’t have that cushion, are at risk, and we will surely see many renewable energy generators going bankrupt soon.”

The solar villain

According to executives, the solution to mitigate curtailment lies in sharing the losses of centralized power plants with distributed generation (DG), concentrated in the solar segment.

The problem is that, although the government is considering including larger distributed generation (DG) plants connected to distributors in the cuts, there is no legal basis to take a similar measure for rooftop photovoltaic panels, which account for the majority of DG.

“Today we have a highly subsidized segment, that of distributed generation (DG), which causes curtailment but does not bear the losses it generates,” says Zanfelice, from Auren. “The balanced solution would be a law defining that energy curtailment , due to oversupply of energy, be distributed among all renewable generators, wind and solar, centralized or distributed.”

According to him, Provisional Measure 1,304/2025, which was supposed to address the problem, was approved by the National Congress and converted into Law No. 15,269/2025 with vetoes and open loopholes regarding the three types of generation cuts.

“The approved legal text, with vetoes, left two points: full reimbursement for past issues up to November and future recognition of curtailment due to reliability ( to guarantee the safety and stability of the electrical grid ), conditional on regulation by Aneel, which has not yet been published,” he says, adding that the Ministry of Mines and Energy opened a public consultation but did not issue a conclusive opinion. “Without rules, companies continue to lack clarity for provisioning and negotiation.”

Mann, from Engie, advocates creating an hourly price signal, similar to the PLD (Price of Energy in the Spot Market) in the free market. "Distributed generation injects energy in the morning, when there is excess supply, so that energy needs to be worth less," he says. "At night, when more expensive thermal plants come online, the consumer doesn't pay extra for it."

The strategies of the energy giants reflect the critical scenario caused by curtailment . In 2025, the excess of solar generation will affect this business model for the first time since 2012, when Aneel created the rules for distributed generation with subsidies.

According to Absolar, the solar market is projected to fall by 29% by 2025, while investments in new projects have declined by 40%. Even solar farms, large-scale installations that produce photovoltaic energy to sell to the electrical grid, have lost their appeal. With double-digit returns until recently, they are now struggling to survive.

The irony is that, in 2025, solar energy remained the second largest source of electricity in the country, with 30 GW of installed capacity, 24.5% of the total, behind only hydroelectric power. For Absolar, the sector's contraction—including both centralized and distributed generation—is directly linked to the losses caused by curtailment .

Isabella Sene, a technical-regulatory specialist at the organization, states that centralized solar power plants suffered losses of R$ 2.8 billion in 2025 in the regulated market alone. "There was also a tax increase: modules that were previously exempt now have a 9.6% import tax, increasing project costs by about 13%," she says.

According to her, the legal uncertainty caused by curtailment led to the closure of companies and job losses. “Large companies and national manufacturers are leaving the market or selling assets,” says Sene, citing Sunco Capital, Light Source, and Next Tracker. “Without new projects, maintaining factories in the country has become unfeasible.”

According to the expert, the biggest challenge for distributed generation (DG) is not the disconnection, but the refusal of connection by distributors, under the pretext of "flow reversal." "There is a lack of transparency about the real capacity of the networks," she says.

While measures remain stalled, the sector continues to face pressure. At the end of last year, taking advantage of a legal loophole, companies requested that Aneel revoke more than 500 permits for new renewable energy plants.

"This case exposes the misalignment between generation expansion and transmission capacity, a growing bottleneck," warns Aquino of Echoenergia.

Casa dos Ventos , one of the giants in the sector, has requested the revocation of permits for 51 power plants, which could produce 2.6 GW of energy. In a statement to NeoFeed , the company affirms that the request is not directly related to oversupply or curtailment .

According to the company, the exclusion of concessions was already part of the planning, and the company seeks to diversify revenues with corporate contracts, self-production, and new markets such as data centers and green hydrogen.

“Casa dos Ventos understands that curtailment is a systemic problem and argues that its solution should not involve penalizing renewable energy generators,” the statement says. “The company actively contributes to the debate on this issue, based on the conviction that Brazil needs to make better use of its natural resources for energy generation.”

for shopping malls.")