In an environment of high interest rates, moderate economic growth, and global uncertainties, the Brazilian market for logistics warehouses follows its own logic.

While sectors more sensitive to credit slow down, industrial and logistics parks maintain high absorption rates, falling vacancy rates, and consistently rising rents.

Behind this disconnect lies an increasingly dominant factor: the rise of e-commerce, driven primarily by Mercado Libre.

A survey by Newmark, obtained exclusively by NeoFeed , shows that the company already occupies approximately 1.8 million square meters (m²) in São Paulo – comfortably leading the ranking of the sector's largest tenants. Amazon, Shopee, and DHL follow, all of which are expanding.

Of an estimated gross leasable area (GLA) of just under 18 million m² in São Paulo, Mercado Livre occupies 9% of the space. And the company, led by Fernando Yunes, maintains its appetite for new areas – in the second half of March it announced an investment of R$ 57 billion in its Brazilian operation in 2026.

One of the recent developments being discussed in the real estate market is the occupation of Avon's headquarters in the southern part of São Paulo. The cosmetics company is transferring its operations to the interior of the state, and the property, which was acquired by the investment firm Goodman, is being converted into a logistics center.

The location, near Interlagos, is a strategic area for supplying the entire southern region of São Paulo. The Australian company, specializing in the acquisition, development, and management of high-quality industrial properties and logistics spaces, has reportedly already signed a contract with Mercado Livre.

At the same time, the Brazilian logistics map is beginning to be redrawn beyond the borders of São Paulo – the state still concentrates about 50% of the national warehouse market.

E-commerce companies and logistics operators are expanding their presence in other regions. The Northeast is advancing, with expansion around the main capitals. The Central-West, especially Goiânia and Brasília, is also registering accelerated growth.

Vitória is emerging as a strategic hub, driven by its port infrastructure and the consolidation of a significant consumer center. And southern Minas Gerais, bordering São Paulo, simultaneously serves the markets of Minas Gerais and São Paulo.

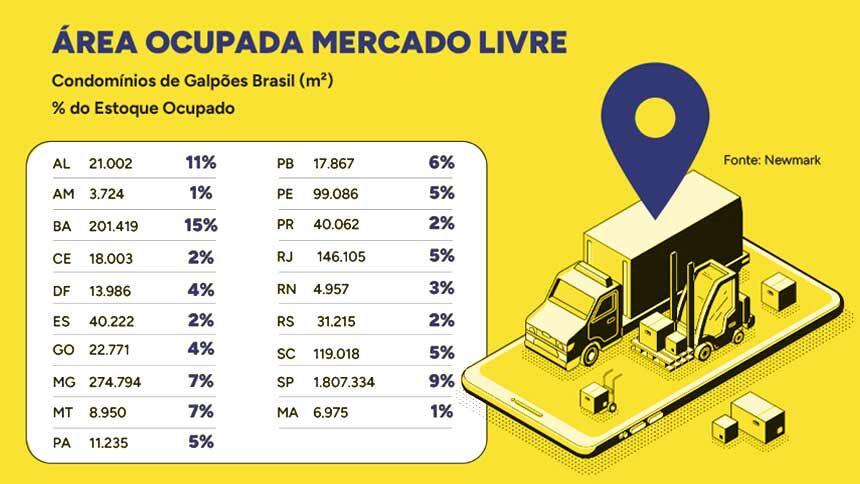

Of a total of 42 million m² of occupied logistics warehouses in Brazil, Mercado Livre accounts for approximately 3 million m² (or 7% of the total).

In Bahia and Minas Gerais, e-commerce occupies more than 200,000 m², which corresponds to 15% and 7%, respectively, of the occupied stock. The states of Rio Grande do Sul, Paraná, Espírito Santo, and Ceará have the lowest percentage of occupied space (2%), ahead only of Amazonas (1%), according to the Newmark study.

"The main driver continues to be e-commerce, and especially Mercado Libre, which is experiencing very aggressive growth," says Mariana Hanania, head of research and market intelligence at Newmark.

"To deliver faster, they need to be closer to consumer markets. Not just in the Southeast region. The expansion is happening all over Brazil," he adds.

This trend of geographic expansion is expected to gain momentum in the coming years, as e-commerce increases its share of retail – which currently still hovers around 10% in Brazil.

Accelerated occupation

The presence of players like Mercado Libre helps explain why the sector started 2026 at an accelerated pace. According to Newmark data, net absorption in São Paulo reached 500,000 m² in the first quarter, a volume six times higher than that recorded in the same period of 2025 and which, alone, already represents more than a third of all absorption last year.

A survey by RealtyCorp Analytics – another study obtained exclusively by NeoFeed – indicates an absorption of 366,000 m² in the same period, reinforcing the same trend of strong demand.

The difference between the data is that Newmark exclusively considers high-end logistics parks (classes AAA, AA, and A) in the state of São Paulo, while RealtyCorp adopts a broader scope, including assets of different standards.

But the prominence of a single brand doesn't tell the whole story of the expansion of logistics warehouses. Operational indicators show a sector pressured by demand from all sides.

The vacancy rate in São Paulo fell to 6.4% - the lowest level in the historical series, according to Newmark - compared to 8.1% in the previous quarter. According to data from RealtyCorp Analytics, which uses a different methodology and sample size, the vacancy rate decreased from 7.35% to the same 6.4% during the period.

In eight of the main regions analyzed by Newmark, availability is already below the state average, a clear sign of relative scarcity, especially in higher-quality assets.

Prices continue on an upward trend. The average asking price for rent reached R$ 33.1 per m² per month, up 3% in the quarter and 15% in 12 months, according to Newmark.

In high-demand areas of the capital (especially within a 30 km radius of the city center), prices already exceed R$ 40 per m², even surpassing the prices charged in tertiary-standard corporate offices.

"The vacancy rate is at its lowest level in the historical series, and demand continues to exceed the delivery of new warehouses. This sustains the price increase and requires strategic planning on the part of companies," says Marcos Alves, CEO of RealtyCorp.

This combination of low vacancy rates, high prices, and high absorption would normally indicate a market nearing saturation. But that's not the case.

There is an explanation for this. Brazil remains an underdeveloped market in logistics. Today, the country has approximately 0.7 m² of warehouse space per inhabitant. In the United States, this ratio exceeds 4 m².

This difference reveals a significant potential for expansion and helps to understand why the sector grows even in the face of adverse macroeconomic conditions.

A survey by Newmark indicates that there are approximately 3.6 million m² under construction in Brazil, with about 1.5 million in São Paulo alone, with deliveries scheduled throughout 2026. Construction activity represents 7.88% of the total stock in the state — a level lower than that observed five years ago, according to data from RealtyCorp.

Five years ago, construction activity exceeded net annual absorption, meaning the market delivered more space than it absorbed. Today, this equation has reversed. Absorption has already accounted for more than 9% of the inventory in the last four quarters, while construction is unable to keep pace.

"We took the data and compared what was being built and what was being occupied five years ago, and we did the same calculation now," says Alves.

"Before, we delivered more than we absorbed. Today, we are absorbing more than is being built. The numbers have reversed, and this points to an even greater scarcity in the future," he adds.

A large part of the projects are concentrated in the main logistics hubs of the state. Cajamar, Guarulhos and the ABCDM region (comprising seven municipalities in São Paulo: Santo André, São Bernardo do Campo, São Caetano do Sul, Diadema, Mauá, Ribeirão Pires and Rio Grande da Serra) are areas that combine proximity to the capital and access to transport infrastructure.

According to Hanania, a recurring trend is expansion within existing condominiums. It's this type of immediate demand that has kept construction activity at a rapid pace. "The tenant who's already there contacts the developer and says, 'I need more units,'" she says.

There is discussion in the market about the potential for growth of the inventory over the next five years. Some projections suggest a doubling of the total size.

Alves is more conservative, but equally categorical. "My bet is that it will grow 50%. But everyone agrees that it will grow a lot. The discussion is about how much."