The Brazilian agribusiness sector is always generating good news, with successive record harvests, high productivity, and frequent increases in its share of the country's trade balance.

However, a previously unpublished report from Banco Inter , which NeoFeed had access to, shows that, beneath the record production figures, a set of simultaneous pressures is eroding margins, cash flow, and the financial health of numerous companies in the sector.

The survey, authored by Rafael Winalda , investment strategist at the bank, cites five conjunctural forces that, combined, form a kind of "perfect storm" for Brazilian agribusiness this year. These include the high price of fertilizers; the bumper harvests in several countries, including Brazil, which drives down commodity prices; and El Niño , which is expected to alter rainfall and drought patterns.

The other two points raised by Inter that form this "perfect storm" in 2026 are high interest rates and corporate leverage, phenomena that are not so recent, but which gain more relevance when combined with the other factors.

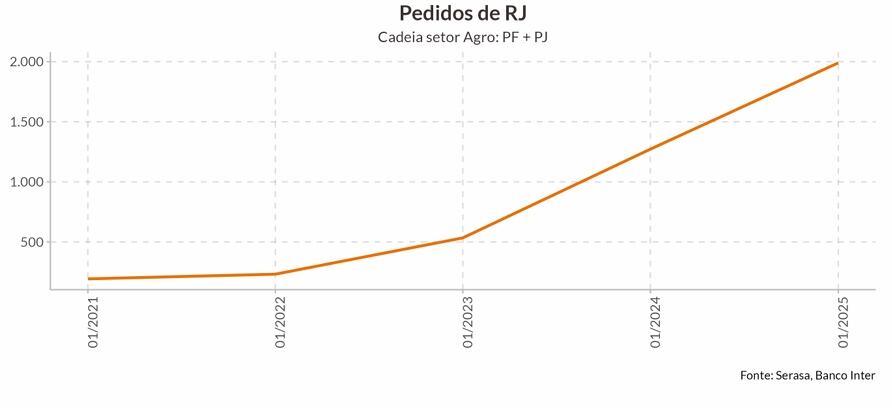

To give you an idea, the number of judicial reorganizations of companies or producers linked to agriculture jumped from less than 500 in January 2022 to more than 2,000 in January of this year.

At Banco do Brasil , the country's largest rural lender, delinquency in its agricultural loan portfolio jumped from 0.6% in December 2022 to 6.2% in March 2026 – a historic peak for the series. To protect itself, the bank increased its provisions for this portfolio to 9.7%, which is exposed to estimated losses of R$ 40.6 billion.

“Although the risk of a systemic crisis is low at the moment, the scenario is alarming, especially for small producers, who suffer more from the perception that credit is more difficult to obtain and more expensive,” says Winalda, in an interview with NeoFeed .

Inter's strategist analyzed each component of this scenario, which individually impacts the sector. Among the risk factors, he cites the rise in fertilizer prices as the biggest cause for concern.

Studies by Comex show that Brazil imports about 80% of all the fertilizers it consumes, a significant number that makes the sector directly dependent on the dynamics of the international market. "Any external shock, whether geopolitical, logistical, or exchange rate-related, is transmitted almost immediately to production costs," he warns.

According to him, the four main fertilizer inputs are urea, ammonium sulfate, phosphate, and superphosphate: "Both urea and phosphate are only at higher levels than in 2022, a year marked by serious distortions in the global supply chain due to the unfolding conflict involving Russia in Ukraine."

Winalda states that a weaker start to the year in terms of urea volume is already noticeable, which may signal a more modest harvest ahead. "On the other hand, there is a clear rush to stockpile phosphate, indicating that the market fears some shortages," he adds.

El Niño effect

El Niño – a natural climate phenomenon characterized by the abnormal warming of the waters of the Equatorial Pacific Ocean – also threatens producers.

Its effects in Brazil manifest themselves heterogeneously: while the South of the country faces intense rains and floods, the North and Northeast suffer from prolonged droughts and water scarcity. In the Southeast, the phenomenon tends to moderate the winter and generate heat waves, without a precise definition between rainy and dry periods.

With El Niño predicted to begin in September, harvests and prices are expected to be impacted at the turn of the year, when the effects will become more evident. "Studies point to the occurrence of a possible Super El Niño this year, an event of exceptional intensity that could significantly amplify all these effects," says Winalda.

For agriculture, this means a greater risk of crop failure, pressure on production costs, and potential water scarcity in irrigated regions, warns the Banco Inter study.

“These factors tend to be directly reflected in the pricing of essential inputs, such as nitrogen fertilizers, whose demand is linked to planting prospects,” the report points out. “In this context, climate monitoring ceases to be merely a meteorological tool and becomes a central element in the sector's risk management.”

Another point cited as a factor in the "perfect storm" in agriculture is the price fluctuation of some of the sector's commodities, which have not been performing as well.

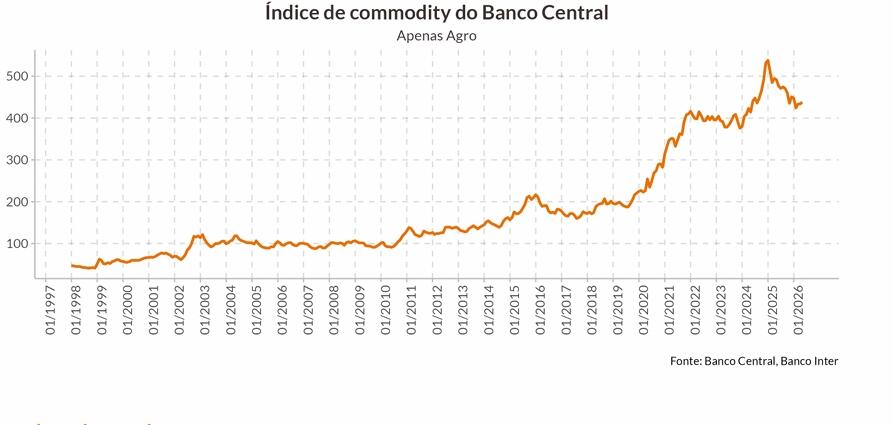

One of the reasons is the combination of simultaneous record harvests in the main global producers. Brazil, Argentina, the United States, and even India are harvesting in historical volumes this cycle, flooding the grain market and putting pressure on soybean and corn prices specifically, even with the sector's aggregate index still at a high level compared to historical standards.

"In practice, this means that the rural producer feels the double effect: the revenue per sack falls precisely at the moment when production costs (fertilizer, diesel, credit) have not yet decreased at the same rate, the so-called scissors effect that has been putting pressure on the profitability of Brazilian agriculture in 2026," the report emphasizes.

The macroeconomic scenario, with high interest rates and inflation above target, also contributes to caution in the sector.

Several factors contribute to this environment: the conflict in the Middle East puts pressure on oil prices, which is transmitted to inflation; concerns about El Niño increase the risk of higher energy and food prices; and variables such as the level of government spending, heated economic activity, and a possible appreciation of the dollar add more noise to the inflationary scenario, keeping the Central Bank in a cautious stance.

"For the agricultural sector, the conclusion is straightforward: expensive credit for longer," the report points out.

The worrying scenario outlined in the report contrasts with the consolidated positive figures for Brazilian agribusiness. Over the last ten years, the sector has accounted for between 23% and 25% of Brazil's GDP, with an upward trend in years of bumper crops and favorable exchange rates.

In 2025 alone, the agricultural GDP totaled R$ 3.2 trillion, growing 12.2% in value and 6.75% in quantity produced compared to 2024. In general, agriculture accounts for half of Brazilian exports of goods, generating 28.6 million jobs across the entire chain, from inputs to agro-industry.

Octaciano Neto , partner at the consulting firm Zera Ag and former Secretary of Agriculture of Espírito Santo, states that the factors pointed out by Banco Inter are indeed concerning in isolation. However, he points out that, despite the specific difficulties, the profitability and productivity of agriculture remain robust.

According to him, the problem is concentrated in specific segments (soybeans and corn) and among more leveraged producers. Therefore, caution is needed when looking in isolation at the growth in the absolute number of judicial reorganizations (RJs) involving individual producers and companies in the sector.

"Brazilian agribusiness has around 5 million rural producers, with 400,000 of them being the largest producers, responsible for 86% of the gross value of production," he says. "On this scale, even though the RJ curve is alarming, the proportion indicates a relatively small segment."

According to him, the increase in judicial reorganizations of rural producers stems from conjunctural factors in recent years. The legislation on judicial reorganization for rural individuals, for example, came into effect in 2021. Since then, the period has been marked by falling prices and rising costs – mainly of fertilizers due to the war in Ukraine, starting in 2022.

Thus, the phenomenon is concentrated in soybeans and corn and among more leveraged producers, not representing a structural crisis in Brazilian agriculture.

The Zera executive argues that, historically, short-cycle crops (such as soybeans and corn) generate a return of 20% to 30% of the invested value in operating profit over 10 years, and long-cycle crops (such as coffee) generate 30% to 40%.

As a result, producers, especially small ones, end up forgetting that commodity prices are cyclical – that is, they are not always sustainable – and end up paying a high price for this exaggerated optimism.

“In 2021, for example, with the price of a sack of soybeans reaching almost R$ 200, with high margins, many producers bit off more than they could chew, taking on commitments and expanding farms and investments, counting on the maintenance of high prices,” he says.

"With the reversal of the cycle, with bumper crops in other countries and falling commodity prices, rising costs and volatility, these commitments became burdensome, leading to cases of financial strain and bankruptcy proceedings," he adds.

Neto states that reducing the number of judicial reorganizations in the sector requires better business management, diversification of financing, and less dependence on public policies, as well as greater emphasis on the financial education of producers and increased professionalization.

According to the Zera executive, financing for the sector has become a "patchwork quilt," with less state involvement over the decades. In this sense, he describes his company as "a tailor of capital": structuring operations for clients, diversifying sources, and seeking funding beyond the balance sheet, working alongside banks, funds, and other capital market agents in financing agribusiness.

According to the expert, small producers still cling to the hope that the government's Harvest Plan can help them. The tragedy, Neto warns, is that the federal government's leading role in agricultural financing has been declining since the 1980s.

“Today, the federal budget contributes less than 1% of the total agricultural credit of approximately R$ 1.1 trillion from this year's Plano Safra; the demand for credit comes from various sources,” he notes, adding that the Plano Safra currently accounts for only about one-third of the annual financing needs of Brazilian agribusiness.

"The other two-thirds are in the capital market and in barter contracts; these are operations that do not involve a single cent from the Treasury," he adds. A barter contract in agribusiness is a form of financing in which the producer exchanges part of their future production for agricultural inputs.

Winalda, from Banco Inter, agrees that the recently announced Plano Safra (agricultural plan), despite its size, is viewed with caution by the sector.

“The perception is that it mainly benefits small and medium-sized producers — those most affected at the moment — but it doesn't solve the structural problem,” says the Inter strategist. “Large companies benefit less and continue to face high costs in the traditional market.”