The Ibovespa started 2026 as one of the major global bets. Fueled by foreign capital inflows, the appreciation of the real, and the international rotation towards emerging markets, the main index of the Brazilian Stock Exchange hit a historic record on April 14th, at 199,355 points, accumulating a 23.7% increase for the year.

Just over a month later, however, the picture of the Brazilian market changed. Since its all-time high, the Ibovespa has fallen 10.9%, reducing its accumulated gain in 2026 to 10.3%, and has become increasingly dependent on a single company out of the 76 that make up the index: Petrobras .

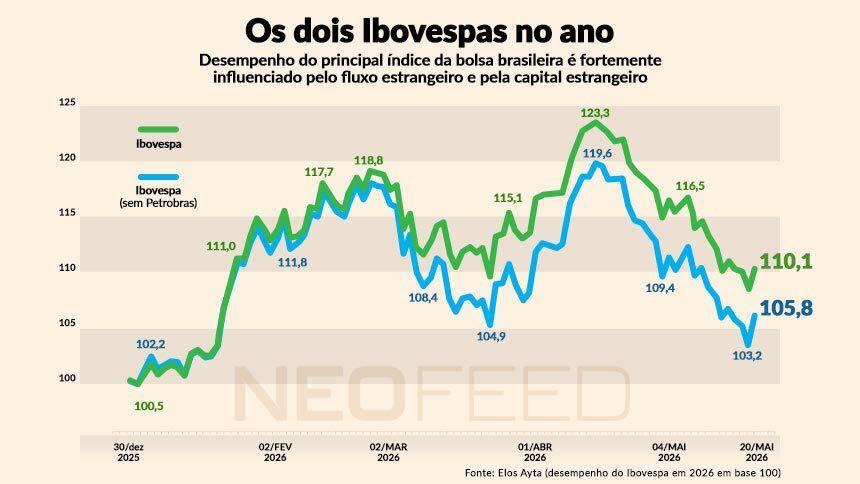

According to a survey conducted by Elos Ayta at the request of NeoFeed , PETR3 and PETR4 shares together account for 22,151 points of the Ibovespa. Since the beginning of the year, the Ibovespa has risen 16,525 points – less than the entire share of the state-owned company in the index this year.

Excluding Petrobras shares from all periods, the Ibovespa would have had a modest increase of 5.8% - accumulating just under 10%. The preferred shares reached a peak of R$ 49.78 on April 13th. From then until the trading session of May 21st, PETR4 fell by about 11%. In other words, the more the oil company's shares fall, the faster the main stock market indicator is pushed into the red.

The concentration of performance helps explain the market's shift in sentiment in recent weeks. Although the Ibovespa is expected to rise in 2026, many of the stocks that participated in the rally have already given back the gains accumulated in the first quarter, while foreign capital, the main driver of the stock market at the beginning of the year, has started to unwind positions almost daily.

The numbers show a reversal in flow. From January 2nd to April 14th, a period in which the index renewed successive records, foreign investors participated in 70 trading sessions and ended only 17% of them with a negative balance. The result was a net inflow of R$ 69 billion into B3.

Since April 15th, however, the trend has reversed. In 23 trading sessions up to May 19th, only two registered a positive balance for foreign investors. In the other 21, the accumulated redemption was almost R$ 24 billion – equivalent to approximately R$ 1 billion per trading session.

At the same time, local investors began returning to the stock market. In the last 20 trading sessions up to May 19, individual investors accumulated a positive balance of R$ 7.8 billion in stock purchases, according to a survey by Argon Investimentos.

The change in hands helps explain why the Ibovespa lost strength even without registering a sharper deterioration in the exchange rate. Since the index retreated from its highs, the dollar has risen from R$ 4.99 to R$ 5.00, while the DXY (an index that measures the US dollar against a basket of strong currencies) has increased by 1.1%.

The resilience of the real also preserved part of the Ibovespa's performance in dollar terms. Even after the recent correction, the Brazilian index has accumulated a 20.5% gain in US currency by 2026.

But, according to experts consulted by NeoFeed , the Brazilian stock market has become small, dependent on a few companies, and vulnerable to foreign investment – without this inflow of capital, its performance will hardly gain traction.

The interest rate factor

While at the beginning of the year the expectation of a drop in the Selic rate and the global search for diversification outside the United States helped sustain the Brazilian rally, the scenario now is almost the opposite.

Economists no longer expect the benchmark interest rate to fall below 13.25% this year, while US stocks have regained momentum after a turbulent start to the year.

"The Ibovespa's rise was unsustainable because expectations of interest rate cuts were reduced by the rise in global interest rates. Brazil cannot go against such a strong global trend," says American fund manager David Wolf.

"The rise in global interest rates has been strengthening the dollar. Normally, this reduces foreign investors' appetite for emerging markets," he adds.

While the Ibovespa has fallen 10.9% since its all-time high, the Nasdaq has risen 11% in the same period. According to Ricardo Campos, CEO of Reach Capital, the recovery of the American market has been driven by a new phase of the artificial intelligence thesis, now focused on hardware and infrastructure companies that lagged behind in the sector's first rally.

"Right now, investors are stopping looking at Brazil and other emerging markets and are going back to buying companies that really have very interesting stories," says Campos.

One of the examples he cited is Sandisk , a memory manufacturer that saw its value increase by nearly 3,000% in 12 months.

The movement helps explain why the Brazilian rally quickly lost momentum. At its peak, Petrobras was already among the main drivers of the index's advance. As of April 14th, PETR3 had accumulated a 61.25% gain for the year, while PETR4 was up 55.35%, a performance close to that of PRIO, which advanced 57.12%.

But the movement still seemed widespread across other sectors of the stock exchange. Following the biggest gains on the Ibovespa were B3, Ultrapar, Assaí, and Auren Energia, with gains of 46.27%, 44.21%, 41.29%, and 40.21%, respectively.

Since then, much of those gains have evaporated. Those who bought these stocks at the peak of the rally have accumulated losses of 14.68% in B3, 3.72% in Ultrapar, 15.17% in Assaí, and 17.73% in Auren Energia. Petrobras shares fell by about 5% during the period, while PRIO still advanced 5%.

According to Campos, the recent correction does not necessarily mean that the Brazilian stock market has exhausted its potential for appreciation. In his assessment, the rise in the Ibovespa index was excessively concentrated in Petrobras and Vale, while a large part of the local companies have not yet undergone a relevant repricing of multiples.

“Many people say that the stock market has already gone up. But there hasn't even been a pass-through of increased company profits to stock prices, let alone a repricing of multiples,” says the CEO of Reach Capital.

The weight of the second semester

At the same time, managers are beginning to give increasing weight to the domestic political scenario. The perception of electoral deterioration has begun to act as a limit to a broader expansion of the Brazilian stock market's multiples.

“Obviously, we had political events,” says Gabriel Spillmann, an analyst at Legacy Capital. “I think the market’s preferred candidate would be a change. And, with the recent scandals, that electoral probability has changed and also contributed to the stock market falling.”

In this context, Petrobras has taken on an unusual role in the Brazilian market: that of protection against global risk. "Any agreement, any continuation of the conflict that leads to a reduction in oil prices, lowering them to US$90 or less, will certainly make the stock market move," says Daniel Utsch, manager at Nero Capital.

Until that happens, the state-owned company continues to function as a kind of geopolitical hedge for the Ibovespa.

“Petrobras, in fact, greatly mitigated the fall in the index. When we think about global macro risk, the main risk factor today is the war in Iran, and Petrobras has developed a negative beta in relation to that,” says Utsch.

"The worse the war, the worse the overall scenario, but the much higher the price of oil, and in the case of Petrobras, the net effect is positive," he adds.

Campos, from Reach Capital, states that this effect already goes beyond Petrobras and is beginning to structurally benefit Brazil itself. "Brazil is a country that gains both in currency appreciation and in revenue from the rise in oil prices," he says.

According to him, the structural change is in Brazil's oil trade balance. "In 2015, our oil trade balance was zero. This year, we're going to have around US$50 billion in positive oil trade balance," he states. "Our entire trade balance last year was US$68 billion. So what's happening with the increase in production and the price of oil is very significant."

For now, the outlook is still positive for foreign investors who entered the Brazilian stock market early. However, the consensus among fund managers is that a consistent recovery of the rally will depend on the return of international capital—especially since foreign investors account for more than 50% of B3's custody and about 65% of the financial volume traded.

According to Wolf, the quickest way to reopen this window of opportunity is through an improvement in the global scenario, even if this reduces some of the specific momentum for Petrobras.

“If the Hormuz blockade is resolved and oil and food prices fall significantly, global interest rates could recover and the market could start thinking about interest rate cuts again,” he says. “The market needs a resolution to Hormuz to start thinking about cuts again. Brazil will follow the global trend.”